This guide caters to four distinct investor mindsets: ‘Capital Preservers’ seeking to protect their wealth; ‘Growth Diversifiers’ wanting to balance their portfolios by diversifying into gold; ‘Tech-Savvy Explorers,’ typically younger investors focusing on digital gold and ETFs; and ‘Inflation Hedgers’ aiming to guard their assets against economic downturns. We tackle key challenges such as inflationary pressures eroding savings, the complexities involved in purchasing physical gold, and concerns about secure storage, laying out a clear path to make well-informed decisions in gold investing.

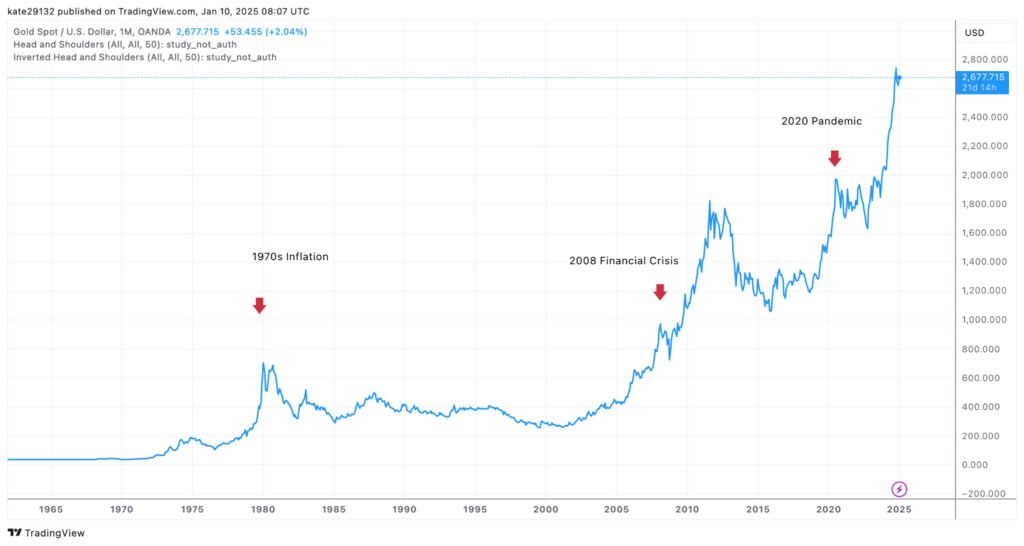

- Key Point 1: Gold serves as an inflation hedge, surging 59% in 2025. However, it remains volatile.

- Key Point 2: Experts suggest allocating 5-15% of a portfolio to gold, weighing storage costs against ETF liquidity. For retirees seeking stability, a conservative allocation closer to 5% may be suitable, helping preserve wealth without excessive risk. Younger investors, who may tolerate greater portfolio volatility, might consider allocating up to 15% to capitalize on the growth potential of digital gold and ETFs. Meanwhile, high-net-worth individuals might strategically allocate around 10% of their assets to gold, benefiting from diversification without overly concentrating their wealth in a single asset class.

- Key Point 3: Physical gold delivers tangible security but requires premiums and insurance; digital options may appeal to tech-savvy users seeking lower entry barriers. For instance, current storage costs can range from $100 to $500 annually. To provide a historical comparison, during the 1970s, storage and insurance costs were significantly lower, often under $50 per annum for a typical investor. At that time, gold traded near $200 an ounce, which underscores the relative affordability of storage costs compared to today’s figures. This contrast highlights how the costs associated with safeguarding physical gold have increased over time, reflecting both past practices and current economic conditions.

- Key Point 4: Gold draws doomsday preppers, but works best as part of a broad, diversified strategy.

- Key Point 5: The debate continues—gold: stabilizer for portfolios, or just a tactical play versus stocks?

Why Consider Gold Now?

Tailoring to Your Needs

Introduction

Understanding the Basics

What Is Gold Investing?

Not Sure If Gold Is Right for You? Before you invest, see how gold fits into a diversified portfolio and what beginners should realistically expect.

Learn How Gold Fits Into Your Portfolio

Types of Gold Investments

- Physical Gold: Coins (e.g., American Eagles) or bars, offering tangible ownership. These forms are ideal for a range of investors. While often preferred by preppers for their security, they are also favored by collectors who value the historical and aesthetic appeal of unique coins. Estate planners might also find physical gold appealing as a tangible asset that can be passed down through generations. However, investing in physical gold involves storage challenges that should be considered.

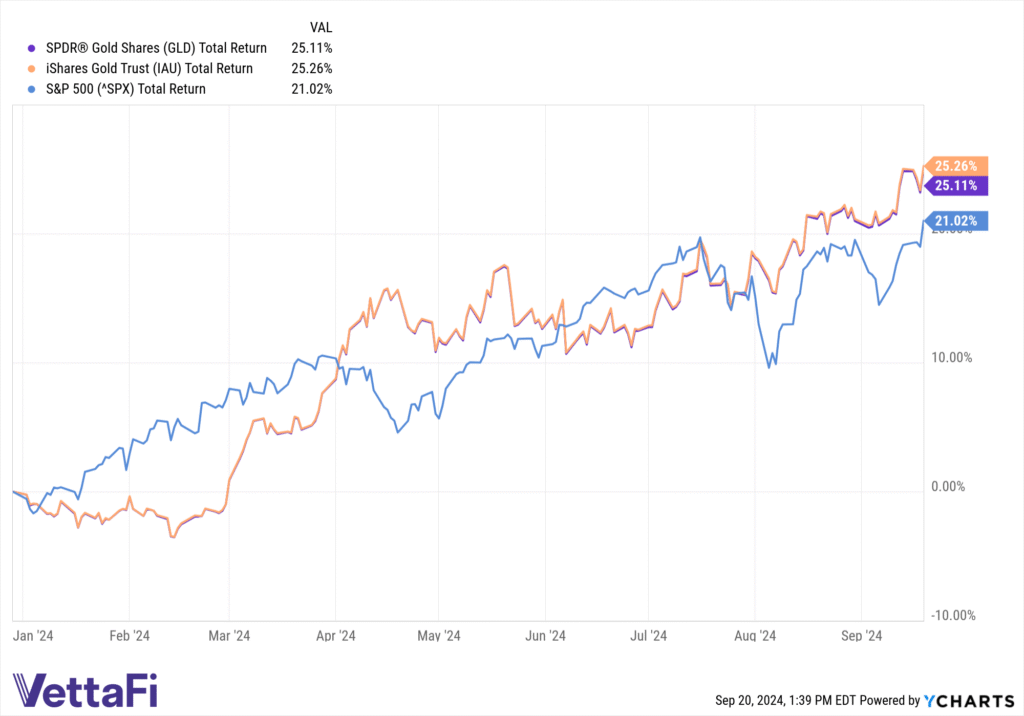

- Gold ETFs: Funds like SPDR Gold Shares (GLD) or iShares Gold Trust (IAU) track gold prices without physical handling. Perfect for tech-savvy investors seeking liquidity.

- Gold Mining Stocks or ETFs: such as the VanEck Gold Miners ETF (GDX), which provides exposure to companies like Newmont. Higher risk but potential for amplified returns.

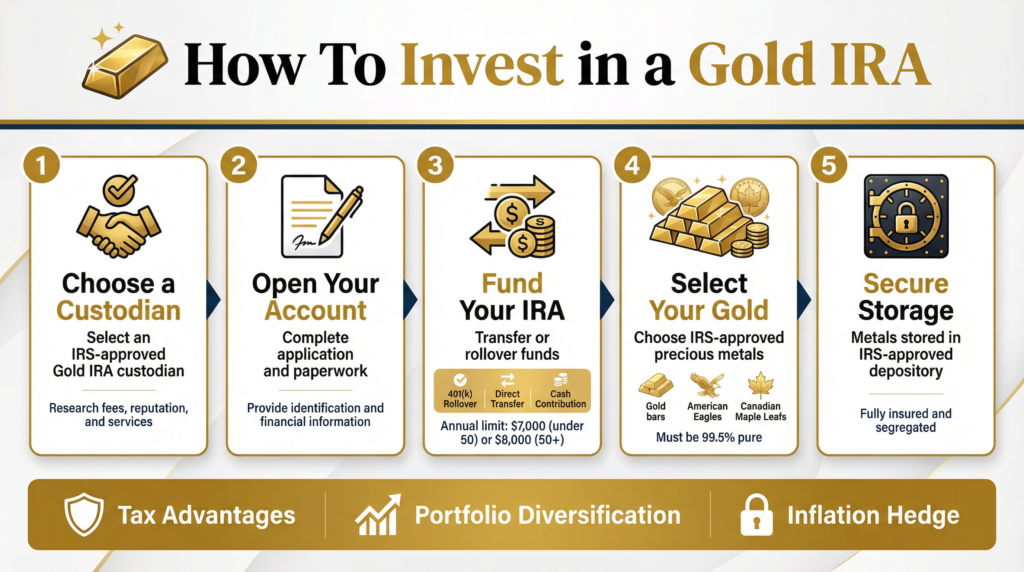

- Gold IRAs: Self-directed retirement accounts holding physical gold, with tax benefits for retirees.

- Digital Gold: Platforms like One Gold and Vaulted offer fractional ownership of vaulted gold. Digital gold provides easy access and instant liquidity, making it simple to buy or sell quickly. Pricing is transparent, and secure storage is managed by reputable firms, freeing you from storage logistics. These features make digital gold attractive to those seeking convenience, flexibility, and cost efficiency without the complexities of handling physical gold. However, investors should be aware of potential risks, such as platform solvency and regulatory oversight. It’s crucial to vet digital gold providers for credibility and security. Look for companies with strong financial backing, apparent regulatory compliance, and robust customer reviews to ensure a safe investment.

Why Gold Fits Your Portfolio

| Physical Gold (Coins/Bars) | Tangible asset, no counterparty risk | Storage/insurance costs, premiums (2-5% over spot) | Doomsday preppers, wealth preservers |

| Gold ETFs (e.g., GLD, IAU) | Low fees (0.18-0.40%), high liquidity | No physical possession, market volatility | Tech-savvy investors, diversifiers |

| Gold Mining ETFs (e.g., GDX) | Potential for higher returns via leverage | Company-specific risks, higher volatility | High-net-worth risk-takers |

| Gold IRAs | Tax advantages, retirement security | Set-up fees ($250+ annually), IRS rules | Pre-retirees/retirees |

| Digital Gold Platforms | Fractional buying, easy storage | Platform fees, digital risks | Younger investors |

Key Considerations

Pros of Gold Investing

In contrast, gold ETFs are taxed at the same rate as other securities, with long-term gains potentially being taxed at a lower rate of 20%, depending on your income bracket. Gold IRAs, meanwhile, offer tax-deferred growth, meaning you won’t pay taxes until you begin withdrawals, typically at retirement. Understanding these tax differences is crucial for effective planning and can help avoid unexpected tax liabilities. Market timing is tricky; over-allocating to gold beyond 15% of your portfolio can expose you to underperformance during bull market periods.

However, gold doesn’t yield income like bonds, and prices can swing (down 10% in short periods). Physical gold incurs premiums (up to 5%) and storage/insurance costs ($100-500/year). Tax implications vary—capital gains on physical gold can reach 28%. Market timing is tricky; over-allocation (beyond 15%) exposes you to underperformance during bull markets.

Economic factors influence gold: Rising interest rates can suppress prices, as seen in early 2023 dips. Counterarguments suggest that gold underperforms stocks long-term (the S&P 500 averaged 10% annually vs. gold’s 5-7%), but for balanced views, it’s not a replacement but a complement.

![]()

When to Invest in Gold

Step-by-Step Guide

Step 1: Assess Your Goals and Risk Tolerance

Step 2: Educate Yourself

Step 3: Choose Your Investment Type

Step 4: Make the Purchase

Step 6: Sell When Needed

Expert Tips

- Diversify Within Gold: Mix physical and ETFs—experts like Blair du Quesnay from CNBC recommend ETFs for liquidity.

- Buy Low, Hold Long: Avoid chasing highs; dollar-cost average monthly purchases.

- Tax Strategies: Use Gold IRAs for deferrals (affiliate CTA: Optimize taxes with a Gold IRA from Augusta)

- Stay Informed: Follow TradingEconomics.com for forecasts—2026 predictions see gold at $4,500+ if inflation persists.

- Secure Storage: For physical, opt for allocated vaults to avoid counterparty risk.

- For Tech-Savvy: Explore the Vaulted app for real-time trading.

- Hedge Smartly: Pair gold with silver for broader metals exposure, per Morgan Stanley.

Common Mistakes

- Not Researching Dealers: Buying from unverified sources leads to fakes. Stick to APMEX or U.S. Mint.

- Overpaying Premiums: Novices pay 10%+ over spot; aim for 2-5%.

- Ignoring Storage Costs: Physical gold can cost $500/year to insure—factor this in.

- Timing the Market: Waiting for “perfect” dips misses opportunities; use averaging.

- Over-Allocating: More than 20% of capital is tied up without income.

- Confusing Gold with Stocks: Mining shares amplify risks—know the difference.

- Neglecting Taxes: Physical sales trigger a 28% gains tax; IRAs mitigate this.

- Falling for Scams: Beware CFTC-warned schemes promising quick riches.

| Overpaying Premiums | Reduces returns by 5-10% | Compare dealers like APMEX |

| Poor Storage Choices | Risk of theft/loss | Use insured vaults |

| Market Timing Errors | Missed gains | Dollar-cost average |

| Ignoring Taxes | Higher liabilities | Opt for Gold IRAs |

| Lack of Diversification | Increased volatility | Mix types within portfolio |

Conclusion

Would you be ready to start? Explore Gold ETFs via a trusted broker. Embrace gold investing as a cornerstone of resilience in 2025 and beyond.

Key Citations

- CNBC: “Gold is on a record run — here’s how to invest, according to experts.”

- Morgan Stanley: “Investing in Gold and Silver: A Decision Guide.”

- NerdWallet: “How to Buy Gold: 4 Ways to Invest In Gold’s Rapid Rise”

- U.S. News: “5 Best Gold ETFs to Buy for 2026”

- Investopedia: “Understanding Gold IRAs: Benefits, Setup, and Risks Explained.”

- CBS News: “5 common mistakes new gold investors make”

- Trading Economics: “Gold – Price – Chart – Historical Data – News.”

Avoid Costly Beginner Mistakes. Many first-time investors overpay on fees or buy from unreliable dealers. The right provider can help you avoid common pitfalls.